In accordance with Art. 161 of the Tax Code of the Russian Federation, organizations can act as tax agents.

The program automates the following cases when organizations can act as tax agents:

- when leasing federal, municipal property or property of constituent entities of the federation from government or administrative bodies;

- when purchasing goods, works, services on the territory of the Russian Federation from foreign organizations that are not registered with the tax authorities of the Russian Federation;

- when purchasing state (municipal) property;

- when selling goods to foreign persons who are not registered with the tax authorities of the Russian Federation on the basis of commission agreements.

Tax agents are required to calculate, withhold from the taxpayer and pay the appropriate amount of VAT to the budget. This section uses an example to examine the reflection of an organization’s business operations when performing the duties of a tax agent when purchasing goods from a foreign organization that is not registered with the tax authorities of the Russian Federation.

To reflect transactions, you must do the following:

1. Registration of an agreement with the performance of duties of a tax agent.

Let's register the agreement in the directory "Contractors' Agreements":

- choose the type of contract - With a supplier,

- check the box "The organization acts as a tax agent for the payment of VAT",

- choose the type of agency agreement,

- Let's indicate the general name.

2. Transfer of advance payment

To do this, you need to register the document “Outgoing Payment Order” (menu “Documents - Cash”).

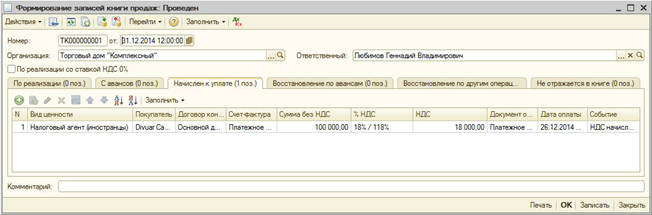

3. Registration of the issued invoice

When transferring payment to a supplier under an agreement with the performance of duties as a tax agent, you must issue an invoice.

An invoice can be generated automatically by processing "Registration of tax agent invoices" (menu "VAT - Registration of tax agent invoices") or entered manually based on the payment document.

Tax agent invoices are generated and posted by clicking the “Execute” button. When processing occurs, invoices are created and the data of previously created invoices is updated.

When posting tax agent invoices, VAT amounts payable to the budget are calculated: an entry is made to the debit of account 76.NA “Calculations for VAT when performing the duties of a tax agent” and to the credit of account 68.32 “VAT when performing the duties of a tax agent.”

The amount of accrued VAT is reflected in the sales book.

In the invoice, the item is filled in with the generic name from the contract. The item name can be indicated manually on the invoice.

4. Receipt of goods

Let's register the document "Receipt of goods and services" with the type of operation "Purchase, commission" (menu "Documents - Purchasing"). To offset the advance payment with the supplier, we will perform the processing “Restoring the sequence of settlements with counterparties” (menu “Documents - Additional”).

Postings are generated:

5. Transfer of VAT to the budget

The fact of VAT transfer to the budget is registered by the document “Outgoing payment order” with the type of operation “Tax transfer” (menu “Documents - Cash”).

The document must indicate the counterparty, the agreement and the settlement document that was used to transfer the payment to the supplier.

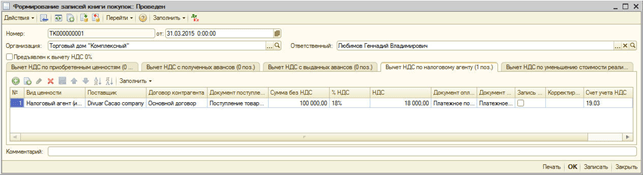

6. Registration of the VAT amount in the purchase book

Purchase ledger entries for VAT deductible amounts when performing the duties of a tax agent are reflected in the document “Creating purchase ledger entries” on the “VAT deduction for tax agent” tab. The table part is automatically filled in using the "Fill" button.

When conducting, the following transactions are generated:

on accounting for VAT when performing the duties of a tax agent for transactions provided for in paragraphs 1-3 of Article 161 of the Tax Code of the Russian Federation (rent or acquisition of state or municipal property, purchase of goods, services from a foreign entity).

Before reading this manual, please read the article in our knowledge base (link below).

Accounting for VAT on transactions provided for in paragraphs 1-3 of Article 161 in the Info-Accountant program can be divided into two stages:

1. The actual issuance of an invoice on behalf of the lessor, a foreign entity (hereinafter referred to as the Supplier) by a tax agent

2. Acceptance for deduction of VAT amounts calculated, withheld and paid by the tax agent

This instruction discusses the option of issuing invoices on behalf of the Property Department, but it is also suitable for purchasing goods and services from a foreign entity.

Registration (issuance) of an invoice by a tax agent on behalf of the supplier

1. The tax agent himself issues an invoice (for the lessor, “agency” invoices) and registers it in the sales book using the form Documentents >> Filling>> >> 2 . Invoice.

It is necessary to issue an invoice on behalf of the supplier (lessor) and indicate the transaction code 06 . To do this, in the “Statement option” field, you must select one of the values: “ for shipment (clause 1-3 of Article 161 of the Tax Code)" or " for payment (clauses 1-3 of Article 161 of the Tax Code)" (Fig.1)

Rice. 1: Window for selecting fields “Statement type” and “Operation type code”

You need to display payment information:

1. If not payment information, That will not be deductible calculated VAT.

2. When entering the payment amount, you must indicate this amount without VAT.

Rice. 2: Example of filling out payment data "Invoice"

Rice. 3: Example of invoice payment postings

After the recalculation, a window of transactions about payment of the invoice by the counterparty appears and the value added tax is highlighted (Fig. 3).

Rice. 4: Window "List of goods and services for the document"

Rice. 5: Example of a printed invoice

Acceptance for deduction of VAT amounts calculated and paid by tax agents

To accept VAT for deduction, you must use the form DOdocuments >> Filling>> 3. Invoices, invoices, invoices, price list>> 18 . Acceptance of VAT deduction by tax agents on transactions provided for in paragraphs 1-3 of Article 161 of the Tax Code of the Russian Federation or standard operation.(Fig. 6)

Rice. 6: Window for setting up the deduction of paid VAT amounts

After selecting this form or operation, a window appears Tax agents: Acceptance of deduction of paid VAT amounts.

In this window the setting option Generate transactions set to value Yes, it can not be changed.

Rice. 7: Invoice selection window

In the table that appears (Fig. 7), add an entry and fill in the fields “Date of acceptance for deduction”, "Acceptance period" And "Register. sf in the book bye.". Field "Acceptance period" not required to be filled in and allows you to create a default distribution of deductions: with the value “ month" - in the next quarter, VAT amounts will be deducted in equal shares for each month of the next quarter, with " quarter» - there will be one entry for the first month of the next quarter for the entire amount of VAT paid.

Field "Register. sf in the book bye." responsible for displaying the invoice one or in a few lines(if, for example, the VAT amount is paid in monthly installments, and the tax agent provides the tax office with a purchase book every month, then the deduction amounts need to be reflected for each month) in the purchase book.

When entering, a table of distribution of deductions automatically appears with the generated data on deductions by default, or empty (if we want to enter the data ourselves). You can independently call up the table of deductions using the “Amount accepted for deduction” field (Fig. 8).

Rice. 8: Deduction distribution table

As a result of this operation, a new business transaction will appear (Fig. 9).

Rice. 9: Window of transactions for deduction

Inclusion of payment amounts into expenses (not a mandatory posting, they are also generated when issuing an invoice, but if you need to include payment in installments as expenses, then fill in the corresponding field in the deductions table). In this case, another business transaction results (Fig. 10).

VAT of the tax agent is taken into account if:

the purchase of goods is carried out in foreign currency from a non-resident;

the property is leased;

the property is for sale.

To account for VAT, accounts 76.NA and 68.32 are used. We propose to analyze all three situations and determine the specific features of the invoice design.

The main condition when purchasing goods in foreign currency from a non-resident is to correctly fill out the contract parameters:

Type of contract – indicate “With supplier”;

The organization acts as a tax agent for the payment of VAT – check the box;

Type of agency agreement – indicate “Non-resident”.

We process the receipt of goods in the standard way, but without registering an invoice:

In the movement of the document, the subaccount 76.NA will be used, and not the usual settlement account.

To reflect VAT, special processing will be used, which can be found on the menu tab “Bank and cash desk” section “Registration of invoices” journal “Tax agent invoices”:

Open the form. You only need to specify the period and name of the agent organization (if the 1C program is used to maintain accounting for several companies at the same time, for example, when using 1C online remotely). Filling out is automatic by clicking “Fill”, and all the necessary documents will be displayed in the tabular section.

By clicking “Run”, invoices will be generated and registered:

In the invoice form, pay attention to the indicated VAT rate - “18/118” and the designation of the transaction code - 06.

The postings will reflect special accounts 76.NA and 68.32, which are added to the chart of accounts:

The amount of VAT for mandatory payment to the budget is checked through the “Sales Book” report and through the “VAT Declarations” document. The “Sales Book” report is generated in the “VAT Reports” section.

In this case, the period of formation and the name of the tax payer organization are indicated:

The VAT return is generated in the “Reporting” section, “Regulated reports”, “VAT return”. The value of the amount for payment will be reflected on page 1 section 2 in line 060:

The tax is paid through standard documents of the 1C program “Payment order” and “Write-off from the current account”, in which the “Type of transaction” - “Payment of tax” must be indicated.

Please note that in order to correctly write off VAT, you must indicate account 68.32.

After this we accept VAT for deduction. Go to the menu tab “Operations” section “Routine VAT operations”.

Create a document “Creating purchase book entries” and open the “Tax Agent” tab:

We post the document and look at the movement in the document “Creating purchase ledger entries”:

Then we move on to creating the “Purchase Book” document, which is located in the “VAT Reports” section. The column “Name of the seller” will appear not as the agent organization, but as the seller organization:

If you look at the declaration, then on page 1 section 3 of term 180 you can see the value of the amount for deduction for the tax agent operation:

The sale of property through a tax agent is formalized indicating the correct type of agreement and in compliance with the fixed assets accounting regulations:

Below is the sequence of registration of invoices by a tax agent:

creation of an agency agreement;

posting of goods or services under the specified agreement;

payment for goods or services to the supplier

registration of tax agent invoice;

payment of VAT to the budget;

acceptance of VAT for deduction through the document “Creating purchase ledger entries.”

In 1C 8.3 configurations, several main types of VAT accounting by tax agents are implemented:

- Payment of VAT when purchasing goods from a foreign company (non-resident)

- Rent

- Sale of property

In the chart of accounts, accounts 76.NA and 68.32 are used to record transactions of tax agents.

Let's consider the features of processing invoices by tax agents.

Payment of VAT when purchasing goods from a foreign supplier (non-resident)

When purchasing imported goods, the main thing is to correctly fill out the contract parameters:

- type of contract;

- attribute “The organization acts as a tax agent”;

- type of agency agreement.

The receipt document is prepared in the same way as for any other goods (Fig. 2), but, unlike ordinary receipt notes, an invoice does not need to be created.

In transactions for reflecting VAT, instead of the usual settlement account, a new subaccount is used - 76.NA.

To generate invoices of this type, processing is used, which is called from the corresponding item in the “Bank and cash desk” section (Fig. 4).

Figure 5 shows the form of this processing.

All invoices issued under agency agreements and paid in the selected period will automatically appear in the tabular section (the “Fill” button, Fig. 5).

Click the “Run” button to generate and register invoices.

The following figure shows the invoice itself (Fig. 6). Note that the VAT rate is selected “18/118”, and the transaction code in this case is 06.

As you can see, the postings (Fig. 7) involve new subaccounts, specially added to (76.NA and 68.32).

The amount of VAT that we must pay to the budget can be checked in the “Sales Book” report and in the “VAT Declaration”.

(Fig. 8) is generated in the “VAT Reports” section

The “Counterparty” column indicates the organization that pays the tax.

Get 267 video lessons on 1C for free:

Generated from the Reporting section. In the “ ” subsection, you need to select the appropriate type (“VAT Declaration”).

Line 060 (page 1 Section 2) will be filled with the amount that needs to be paid to the budget (Fig. 9).

Payment of tax to the budget is formalized using standard 1C documents (“Payment order” and “”). Both documents must have the type of transaction “Payment of tax” (Fig. 10).

When writing off money, it is important to indicate the same account as when calculating tax - 68.32 (Fig. 11).

Finally, you can accept VAT as a deduction. Transactions are created by the document “Creating purchase ledger entries”:

Operations –> Regular VAT operations –> Generating purchase ledger entries –> “Tax Agent” tab (Fig. 12).

After posting the document “Creating records...” (the transactions are shown in Fig. 13), you can create a purchase book. This report is called similarly to the “Sales Book” report from the VAT Reports section.

In the column “Name of the seller” it is not the agent that appears, but the seller himself (Fig. 14).

In section 3 of the VAT return (Fig. 15), amounts will appear that can be deducted for transactions of tax agents.

Renting and selling property

Registration of VAT transactions when selling property and leasing municipal property has no fundamental differences from the above scheme.

The main thing is to choose the right type of agency agreement (Fig. 16).

In addition, when drawing up a document for capitalization of rental services, you must correctly indicate the accounts and cost analytics (Fig. 17).

The wiring is shown in Fig. 18. They also have a special account 76.NA.

In what order is an invoice issued when a Russian buyer performs the duties of a tax agent? We pay a foreign organization for a trademark, thereby acting as a tax agent for the payment of VAT to the budget. How are invoices received and invoices issued filled out?

In this case, the received invoice is not filled out.

When drawing up invoices, the Russian Ministry of Finance recommended making a note on them “For a foreign person” (letter dated May 11, 2007 No. 03-07-08/106).

In line 2 “Seller” of the invoice, your organization must provide the full or abbreviated name of your organization (specified in the agreement with the tax agent) for which you fulfill tax payment obligations.

Line 2a “Address” must indicate the address (in accordance with the constituent documents) of the seller (specified in the agreement with the tax agent) for whom you are fulfilling the obligation to pay tax.

In line 2b “TIN/KPP of the seller” there must be a dash.

In lines 3 “Consignor and his address” and 4 “Consignee and his address”, tax agents purchasing work (services) from foreign organizations put dashes.

In line 5, indicate the number and date of the payment document confirming the transfer of the withheld VAT amount to the budget. In line 7 “Currency: name, code” indicate the name of the currency according to the All-Russian Classifier of Currencies and its digital code

In case of partial payment, dashes are placed in columns 2–4, and columns 10–11 are not filled in.

The rationale for this position is given below in the materials of the Glavbukh System

1.Situation:How to fill out an invoice as a tax agent

In line 2 “Seller”, tax agents purchasing goods (work, services) from foreign organizations that are not tax registered in Russia (clause 2 of Article 161 of the Tax Code of the Russian Federation, clause 3 of Article 161 of the Tax Code of the Russian Federation), provide the full or abbreviated name the seller or lessor (specified in the agreement with the tax agent), for whom they fulfill tax payment obligations.*

Line 2a “Address” must indicate the address (in accordance with the constituent documents) of the seller or lessor (specified in the agreement with the tax agent) for whom the tax agents fulfill the obligation to pay tax.

In line 2b “TIN/KPP of the seller” the following must be entered:

- dash – if the invoice is filled out by a tax agent purchasing goods (work, services) from a foreign organization that is not registered with the tax authorities in Russia (Clause 2 of Article 161 of the Tax Code of the Russian Federation);*

- INN and KPP of the seller or lessor (specified in the agreement with the tax agent), for whom the tax agent fulfills the obligation to pay tax, in all other cases (clause 3 of Article 161 of the Tax Code of the Russian Federation).

When drawing up an invoice for work performed (services rendered) in lines 3 “Consignor and his address” and 4 “Consignee and his address”, tax agents purchasing work (services) from foreign organizations that are not tax registered in Russia (p 2, Article 161 of the Tax Code of the Russian Federation), as well as tax agents leasing state or municipal property directly from state authorities and local governments or acquiring (receiving) state or municipal property on the territory of Russia that is not assigned to state (municipal) organizations (p. . 3, Article 161 of the Tax Code of the Russian Federation), put dashes.*

The procedure for filling out line 5 “To the payment and settlement document” has some peculiarities.

When purchasing works (services) from foreign organizations that are not registered in Russia for tax purposes, in line 5, indicate the number and date of the payment document confirming the transfer of the withheld VAT amount to the budget.*

In line 7 “Currency: name, code”, indicate the name of the currency according to the All-Russian Classifier of Currencies and its digital code* (subparagraph “m”, paragraph 1 of Appendix 1 to). If in the contract the price of a product (work, service) is indicated in foreign currency and its payment is also made in foreign currency, the tax agent can draw up an invoice in foreign currency (Clause 7 of Article 169 of the Tax Code of the Russian Federation).

When filling out the invoice columns, tax agents purchasing goods (work, services) from foreign organizations that are not tax registered in Russia (clause 2 of Article 161 of the Tax Code of the Russian Federation), as well as tax agents leasing state or municipal property directly from bodies of state power and local self-government or those acquiring (receiving) state or municipal property on the territory of Russia that is not assigned to state (municipal) organizations (clause 3 of Article 161 of the Tax Code of the Russian Federation), must adhere to the following rules.

When full payment is made for goods (works, services), the invoice columns should be filled out in the manner prescribed by paragraph 5

In case of partial payment, dashes are placed in columns 2–4, and columns 10–11 are not filled in.*

For both full and partial payment (including non-cash payments), please indicate:

- in column 1 - the name of the goods supplied, property rights (description of work, services);

- in column 7 - the estimated tax rate (10/110 or 18/118) or the entry “Without VAT”;

- in column 9 - the sum of the indicator in column 5 and the indicator calculated as the product of the indicator in column 5 and the tax rate of 10 or 18 percent, divided by 100;

- in column 8 - the amount of tax calculated as the product of columns 9 and 7, in rubles and kopecks without rounding (letter of the Ministry of Finance of Russia dated April 1, 2014 No. 03-07-RZ/14417);

- in column 6 - the amount of excise tax, and if the product is not excisable, then indicate “Without excise tax”.

This procedure for filling out invoices is established in Appendix 1 to Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137.

After filling out all the required details of the invoice drawn up on paper, it must be signed by the head and chief accountant of the tax agent organization (other persons authorized to do so by order of the head or by a power of attorney on behalf of the organization). If the tax agent is an entrepreneur, he must personally sign the invoice and indicate in it the details of his registration certificate. This procedure is established by paragraph 6 of Article 169 of the Tax Code of the Russian Federation.

With regard to the preparation of previous forms of invoices, similar explanations were contained in the letter of the Federal Tax Service of Russia dated August 12, 2009 No. ШС-22-3/634.

When calculating tax, as well as when issuing an advance (partial payment), including in non-monetary form, tax agents purchasing goods (work, services) from foreign organizations that are not tax registered in Russia (clause 2 of Article 161 of the Tax Code RF), as well as tax agents leasing state or municipal property directly from state authorities and local self-government or acquiring (receiving) state or municipal property on the territory of Russia that is not assigned to state (municipal) organizations (clause 3 of Article 161 of the Tax Code RF), draw up an invoice and register it in the sales book (clause 15 of section II of Appendix 5 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137). When presenting VAT for deduction in accordance with paragraph 3 of Article 171 of the Tax Code of the Russian Federation, previously issued invoices for advance payments (partial payment) are registered in the purchase book (clause 23 of section II of Appendix 4 to Decree of the Government of the Russian Federation of December 26, 2011 No. 1137).

Olga Tsibizova

2.Situation:How to draw up an invoice for a tax agent if he purchases goods (work, services) from a foreign organization that is not tax registered in Russia

Draw up an invoice in the manner established by paragraphs 5.1 and Article 169 of the Tax Code of the Russian Federation, taking into account some features.).*

At the same time, some items of invoices prepared by tax agents are filled out in a special order. For example, in line 2b “TIN/KPP of the seller” you need to put a dash (clause 1 of Appendix 1 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137). In relation to filling out previous forms of invoices, as additional information, the Ministry of Finance of Russia recommended making a note on them “For a foreign person” (letter dated May 11, 2007 No. 03-07-08/106).*

An example of drawing up an invoice by a tax agent when purchasing services from a foreign organization. A foreign organization is not tax registered in Russia

Alpha LLC (customer) entered into an agreement with the Ukrainian organization Lawyers of Ukraine (executor) for the provision of legal services that are necessary for production activities subject to VAT. The cost of services under the contract is USD 11,800, including VAT. A Ukrainian organization is not registered for tax purposes in Russia. The place of sale of legal services is Russia (subclause 4, clause 1, article 148 of the Tax Code of the Russian Federation). Consequently, their value is subject to VAT.

Services were provided between March 13 and March 15. On March 15, the parties signed an acceptance certificate for the services provided. On the same day, Alpha’s accountant transferred the payment to the Ukrainian organization and drew up an invoice marked “For a foreign person.” At the same time, when filling out line 2b “TIN/KPP of the seller” of the invoice, the Alpha accountant added a dash. The amount of VAT that Alpha must withhold from the income of the Ukrainian organization as a tax agent is USD 1,800 (USD 11,800 ? 18/118). VAT withheld from the income of the Ukrainian organization was transferred to the budget by payment order. The Alpha accountant indicated the details of this payment document in line 5 of the compiled invoice.

The following entries were made in Alpha's accounting.

Debit 26 Credit 60

– 330,000 rub. ((USD 11,800 – USD 1,800) ? 33 rubles/USD) – costs for legal services provided are reflected (based on the acceptance certificate);

Debit 19 Credit 60

– 59,400 rub. (1800 USD ? 33 rubles/USD) – VAT is taken into account on the cost of services, which is subject to withholding when paying income to a Ukrainian organization;

Debit 60 Credit 68 subaccount “VAT calculations”

– 59,400 rub. – VAT is withheld from the amount payable to a Ukrainian organization that is not tax registered in Russia;

Debit 60 Credit 52

– 330,000 rub. – payment to the Ukrainian organization is transferred (minus withheld VAT);

Debit 68 subaccount “VAT calculations” Credit 51

– 59,400 rub. – the amount of withheld VAT is transferred to the federal budget;

Debit 68 subaccount “VAT calculations” Credit 19

– 59,400 rub. – accepted for deduction of VAT, withheld from income payable to the Ukrainian organization and transferred to the budget.

Olga Tsibizova, Deputy Director of the Department of Tax and Customs Tariff Policy of the Ministry of Finance of Russia

- Download forms